What can merchants do to accept mobile payments in a secure manner?

Want to learn more about mobile payment and how merchants accept it? This blog is for you.

What is Mobile Payments?

In a broad sense, mobile wallets are any technology. That converts your smartphone into a money-saving device capable of facilitating financial transactions. It could also include credit card transactions using near-field communication technologies (“tap to make a payment”). And usually provides incentives for customers, like loyalty programs or coupons.

The primary benefit has to do with “contactless payments,” which typically involves NFC technology. Mobile phones like those like the Samsung Galaxy S20 use NFC therefore you don’t need to swipe your credit card. Instead, you place the phone over an reader that scans the QR code of the card of the user. This is a leading feature of digital wallet app development.

Mobile wallets can be used in the retail store to facilitate small-scale business transactions however, they are also able to be used to make online payments. This allows customers to not carry an actual purse or wallet, by using the same device for all transactions.

Naturally, mobile wallets will complete the transaction by using the customer’s credit card. For instance, they could connect Apple Pay to their bank card or credit card. The sensitive card information is replaced by encrypted tokens to ensure extra security.

With a variety of digital wallet applications smartphones is able to pay for purchases to save loyalty points to redeem. And replace papers boarding passes, carry personal identification and send credentials to allow access to locked rooms and doors.

The types of payment made by mobile phones

Before your hire dedicated developers, let’s look at the different types of one mobile payment types.

-

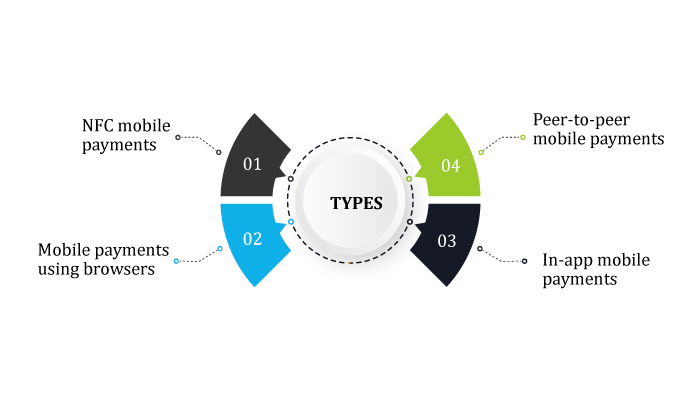

NFC mobile payment

NFC payments enable wireless data transfer between devices in proximity to each the other. Mobile payment platforms such as Google Pay, Apple Pay as well as Samsung Pay use NFC technology. This is to make contactless transactions possible across the world.

Certain countries are beginning to utilize NFC technology that goes beyond payments processing to prove identity. There is no need for standard chip technology , nor credit or debit card.

-

Mobile payment using browsers

Mobile payments that are based on browsers facilitate the use of cards not presented (CNP) transactions online. When you go to the mobile checkout page it allows you to enter the payment details to complete the transaction.

If you’ve ever purchased something on the internet, you’ve probably made use of mobile payments that are based on browsers. The built-in interface makes checkout process simple and quick.

-

In-app mobile payment

Mobile payments in-app are precisely as they sound. They’re electronic payments which you can use within an application. In-app payment makes it simpler for companies to sell their goods and services within the app’s ecosystem, which they manage.

All you need to do is sign up with your payment details to start making purchases. Anything you can imagine is available for purchase in the app. That results in more enjoyable user experience as well as higher conversion rates. This also removes the requirement to quit the app to purchase items.

-

Peer-to-peer mobile payment

Peer-to-peer transactions, also known as P2P transactions, are transfer between two individuals. They can be enabled by using platforms such as Venmo and PayPal. And allow users to transfer money using their mobile devices.

After your bank or credit card details are set, you can pay your debtors money or split purchase payments with your family members. Or split payments together with others.

Pros and negatives of digital wallets

Mobile banking app development has it’s own ups and downs. So let’s look at them here.

-

Pros of mobile payment:

Convenience It’s much easier in carrying and helps free up pockets space, as it’s available through your smartphone. Furthermore, you can keep different types of cards in your digital wallet.

Additional backup You can pay at a variety of retailers in the event that you lose your wallet.

Security Digital transactions have added security in the form of tokenization and encryption of data. That makes them more secure in different ways as compared to traditional credit or debit card transactions.

-

Cons of mobile payment:

Certain limitations on the places you are able to utilize it It is not possible for every store or individual you wish to transfer money to accepts transactions made via digital wallets. Or does not have the technology at the moment to make it possible.

It depends on the device you use When the device where your digital wallet’s storage. It will run out of power, or you are unable to access it due to some reason. This means losing access to your digital wallet.

What information can An App Receive?

People often ask, what information does eWallet app development services take. Here’s a view of that.

- Your contact details, including your name, postal addresses, email address and your mobile number.

- Recordings of your calls and texts.

- Your contacts.

- Your calendar.

- Your unique identification number for your mobile device.

- Information about your account.

- Websites that you visit with the mobile phone.

- Your location , as well as where you shop or go on the mobile phone.

For mobile payments, apps can also gather information about the places you shop, the items you buy and how much you spend, as well as the coupon codes and loyalty program you are a part of.

Certain mobile payment apps do not collect or disclose the data necessary to process the transaction however, other apps may gather additional details about you. The apps may utilize your personal information to serve reasons unrelated to making a payment, like to offer you features within the app or to advertise for other companies. They may be able to share information about your private data with other businesses.

Who else could gather information through your use of a credit card application? This could include the store or an advertising network, a data broker that gathers information about users from many data sources before packaging it up for sale, the maker of the mobile phone, your payment service provider (such the credit card company you use) as well as a payment processor as well as your wireless carrier, broadband service provider, as well as the companies that you pay.

What’s the advantages of mobile wallets to businesses?

-

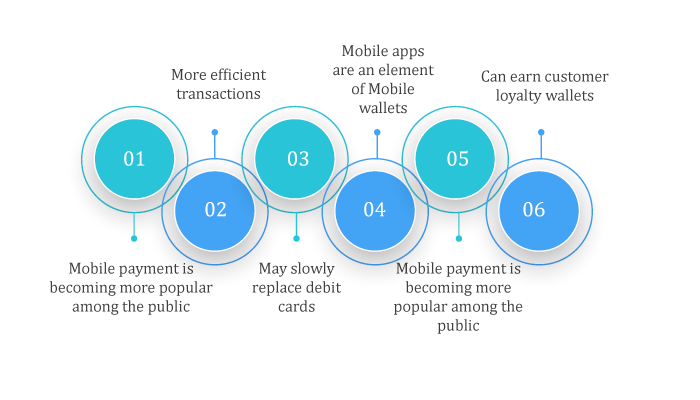

Mobile payment is becoming more popular among the public.

A report in November 2020 about mobile payment forecasted that by the year’s end more than 760 million people worldwide will be customers of mobile wallets. With such a huge number of users, it is logical for your business to accept mobile payments . More convenience for your customers could mean greater sales for you.

-

More efficient transactions.

Mobile wallets allow for faster transactions than traditional ones such as credit and debit cards. The debit cards require the user to enter a PIN number and credit cards could require customers to sign their signature before the transaction is completed, but neither of these requirements are part of mobile wallet transactions.

-

May slowly replace debit cards.

Mobile wallets are generally an extension of debit cards, rather than completely new bank accounts that users open to be able to make payments through their mobiles. They could be able to replace completely debit cards. This is especially so since most Generation Z or Generation Z customers always have their phones on them, and abandoning a wallet or credit card in the house isn’t an issue for this demographic.

-

Mobile apps are an element of Mobile wallets.

Check out Starbucks to see the best example of this feature in practice. Starbucks is a ubiquitous brand that provides rewards programs, coupons, and more incentives via its app that can be linked to the mobile wallet of a customer and utilized as a payment method that can be thought of as a virtual Starbucks card. This system simultaneously offers Starbucks the ability to offer a rewards program as well as a payment option via which 25 percent of its transactions take place.

-

Extra security.

Credit cards are prone to security concerns and many of them are removed when you use mobile wallets to make payment. For instance, since mobile wallets have to be authenticated by the user with a fingerprint or four – to six-digit PIN that they provide, you do not need to be concerned about staff members not being able to match the client’s signature or name with the one on the card. It’s also not possible to accepting fake credit cards because without connections to a valid debit account mobile wallets and payment apps do not work.

-

Can earn customer loyalty.

Certain customers are set on paying only using mobile wallets. If your business is one of few in your sector or market that accepts mobile payments, they will most likely select you over a rival.

How do mobile payments work?

Most mobile payments are based upon Near Field Communication also known as NFC technology. Simply put, NFC allows two devices which are close to exchange data. For mobile payments, transactions are made using devices for consumers like tablets or smartphones as well as a merchant device such as the credit card terminal.

A majority of people will be able to have access to this feature through built-in mobile wallets that are available on smartphones. Mobile wallets are an application that stores the details of credit and debit cards to allow users to pay for things electronically. In order to use an mobile wallet, users can safely add their credit or debit card details to a mobile wallet application. The majority of mobile wallets require a fingerprint or facial recognition authentication to ensure that transactions are not fraudulent.

Alternately, mobile payments can be accepted with the help of QR codes customized to the customer’s needs. In these cases it is the user’s device that generates the QR code that contains the details about the payment. The merchant uses the payment system for scanning the QR code and then complete the transaction.

Are mobile payment systems secure?

Securely protecting customer data is an essential concern for companies today in this 21st century.

The positive side that payment transactions on mobile devices that uses NFC technology is among the safest methods for individuals to shop. When a user swipes their debit or credit card, the bank details are recorded and sent to networks. But, NFC technological mobile payments use tokenization to minimize the risk for data loss.

That means that when customers use his mobile to make a purchase it creates an individual-use card number to make the purchase. The unique number is transferred to the POS system used by the merchant to process the transaction. In this way, merchants are not required to handle or manage sensitive customer data.

Furthermore it is true that mobile devices do not typically store transactions information within the processing. Instead, the unique credit card numbers are generated by a secure chip that is installed on the device, and is distinct from the tablet’s or smartphone’s CPU. The card’s information is saved in the cloud. It may be deleted remotely, in the event of need.

To provide additional security mobile wallets need customers to confirm their identity prior to making a purchase. This can be accomplished through biometric data recognition , like the scanning of fingerprints or unlocking the device with an individual numeric code. Although no method of payment can be completely secure mobile payments are the most secure payment methods for both consumers as well as merchants because of the multiple layers of security measures.

-

Tokenization

Tokenization is a technique that is able to promote mobile payments while also protecting personal information of customers from hackers and other cyber-security threats.

If a system for storing data at a store is compromised due to an attack from cyberspace, hackers are able to gain access to tokenized data. The data that is tokenized is inaccessible to cybercriminals because the customer’s data is secured by an unintentionally generated token. Mobile wallets do not send the card’s primary account number (PAN) like is the case when you pay using a credit card. In a mobile payment transaction the token is transferred through the POS terminal, which protects the information while it is in transit.

-

Cryptograms that are specific to the device

This method ensures that the transaction originated directly from the device used by the cardholder. If hackers were able to steal information during a mobile payment transaction, the cryptogram which is sent along with the token to the POS terminal cannot be transferred to a mobile device because it is exclusive in the initial.

-

Two-factor authentication

Also called ‘2FA’ this type of security makes use of two methods of identification for authentication. It could be an amalgamation using a password phone or credit card or a biometric system like fingerprints, facial recognition or voice.

The advancements in technology for payments are a few of the elements that make the possibility of mobile payments attractive both to vendors and consumers because both parties is safe from cybercrime and fraud.

Advice for buildering merchants interested in mobile payment wallet

-

AREA OF THEIR OWN MOBILE ACCEPTANCE SOLUTIONS

Utilize a certified POI (POI) Technology Mobiles are not always intended to be secure input devices and storage systems for the cardholder’s data. Mobile payment solutions therefore requires additional technology, such as encryption to protect acceptance of cardholder data.

The first component of a secure mobile payment option is an accepted “point of interaction” this is the tech name for an authorized PIN entry device (PED) or an approved security card reader (SCR) that is used to collect and decrypt the cardholder’s data to secure the purpose of completing a transaction.

For instance, the picture above illustrates two options which are: one is an Secure Card Reader (SCR) which is used to scan the magnetic stripe on an account; the alternative is a PIN Entry Device (PED) to read the card and entering the PIN. These devices all have one purpose in mind: securely capture and encode information of the cardholder. When more devices are accepted and listed on the website of the Council.

-

Follow your compliance with PCI Data Security Standard

One of the major benefits that comes with using a valid P2PE system for secure mobile transactions is the scope reduction. This means that a valid and well-implemented solution for processing mobile payment may reduce the requirements that you must meet for annual compliance as a merchant in accordance with PCI DSS. Reduced scope can drastically reduce the cost and work involved in compliance. Still, you are responsible for ensuring compliance with the PCI DSS requirements regarding business policies and procedures and contract agreements in conjunction with the P2PE supplier, as well as physical protection of the assets of your payments and for ensuring that you follow guidelines in the P2PE instructions in the Manual.

5 main factors that are driving mobile payments

If you want to develop eWallet app like Klarna, here are some factors that you need to consider.

-

The smartphone has grown beyond phones.

Smartphones have not only changed our lifestyles and work but also the way we communicate with each other as individuals as well as with companies. According to Statista the amount that smartphone owners use across the U.S. has continued to grow steadily over the past several years. At present more than 80percent of U.S. households own a smartphone and the forecasts indicate that smartphone use across North America will continue to grow steadily into the future.

The rise in smartphone ownership has resulted in a surge in the development of mobile apps and use. In reality, eMarketer estimates mobile app usage accounts for around 88% of the total digital media consumption. 3 In addition, the expansion of the market for mobile apps has resulted in increasing mobile payment in both the B2B and B2C payments sector.

Mobile payments offer consumers an effortless and seamless method to make purchases online and at the point of sale and pay bills. It also allows you to transfer money. Merchants as well as individuals have taken to app-based commerce as well as in-app payment. Businesses are rapidly increasing their investment in mobile applications for their employees, with new ways to provide the user with a seamless payment experience.

-

The younger generation is driving mobile payments adoption.

While the use of smartphones has grown over all generations it’s the younger generations who are driving the rapid growth of mobile payments. The younger generation is taking on decision-making roles at work.

As per research by the Pew Research Center, roughly 93 percent of Millennials and 93 percent of Gen Xers have smartphone. Generations that are in this generation comprise the majority of mobile payments that are made. They are frequently motivated to make use of mobile payments due to the possibility to get discounts, rewards or alerts. They also have electronic receipts as well as the convenience and convenience that mobile payments bring.

Gen Z, those born after 1996, is moving the payment system towards more mobile and peer to peer transactions (P2P). Gen Z, like Millennials have high expectations of mobile experience and are more comfortable than the other generations when it comes to moving money electronically. As the use of digital devices rises the ways that everyone interacts with money both at home and at work will evolve as more people switch to debit, cash, and credit cards to mobile payment.

-

Technologies have made it easier to make more secure and convenient payments.

Prior to the smartphone was invented, there was the need to strike the right equilibrium between convenience and security when it comes to payment innovation. This is the reason for the introduction of credit and debit cards, and then the widespread use of PIN technology as well as using the EMV (r) chip, and finally mobile wallets as well as credit cards that are contactless.

Mobile wallets are a convenient and secure method of paying for both goods and services. By using a wallet on the go consumers can save their consumer and corporate credit card details on their smartphones to later access. Tokenization lets users save their credit card details inside their mobile wallets in a secure manner. Tokenization substitutes the credit card number, making the data unusable to thieves.

With a stronger security layer mobile wallets are much more secure and speedier when compared to a traditional credit card. When shopping in stores, customers simply place their phone in proximity to the point-of-sale (POS) machine. Credit card details are immediately and safely shared with the POS device by using near-field communication (NFC) technology.

In a growing number, modern payment devices and solutions reduce the possibility of data breaches, and the consequent financial and reputational damage through improved security of payment data.

-

The COVID-19 pandemic

Prior to the outbreak, prior to the outbreak, U.S. was slow to accept mobile payments. Despite the prevalence of smartphones however, there was a slow adoption of mobile payments. U.S. has a strong habit of using credit cards. The epidemic prompted major modifications to how products and services were bought.

In the wake of the epidemic and people became more apprehensive about the health risks that come dealing with cash and checks or handing over a credit card to cashiers or touching the POS machine. Mobile wallets, as well as contactless cards, offer an alternative that is safer than traditional credit cards because they don’t require the touch of the POS machine to input the PIN.

This has led to a rise in the demand for contactless payment in retail stores such as supermarkets as well as restaurants that can help lower the risk of transmission, has increased dramatically. Based on the 2022 Global Payments Report, credit card use is changing and is transferring via mobile wallets. Mobile wallets’ percentage of POS transactions increased significantly in 2021 and grew to 28.6 percent of the total POS transactions, which is more than US$13.3 trillion. The usage of mobile wallets at POS is growing quickly, it seems that the patterns that were developed during the outbreak are here to endure.

-

Change is being driven by merchants.

Merchants also gain by mobile transactions. Like people, mobile payments offer enhanced security for payments, faster checkout speeds and more information to monitor trends in customer behavior and inventory. These advantages make it easier for businesses to allow mobile payment. To encourage customers to pay with mobile some merchants offer discounts as well as other incentives in order to show their value to consumers. Certain merchants have successfully integrated mobile payments and loyalty programs inside their mobile payment applications. Customers are able to earn rewards points and coupons, and other perks such as mobile order.

14 mobile payment solutions for businesses

Let’s look at some of the best examples of top fintech apps in this section of the blog.

1. PayPal Zettle

PayPal Zettle is a point-of-sale all-in-one solution for small-sized businesses. It can be used either in-store or mobile. Pay with any payment method (cash cards, chip-cards and contactless) and monitor sales and inventory anywhere using the PayPal Business account. Cost: 2.29% + 9C for each transaction.

2. Square

Square allows you to take payment in-person, while on the go or via the internet. Make and send invoices and then let customers pay using a debit or credit card. ACH or bank transfer. Include delivery and pick-up choices, and sell via social media. Square’s hardware options for point of sale transactions are terminals as well as a reader that can read chip and contactless, as well as magstripe readers. Cost: 2.6% + 10C(in-person), 2.6% + 10C (in-person), 2.9% + 30C(online), 2.9% + 30C (online) per transaction.

3. Google Pay

The Google Pay is an online wallet that is digital and a payment system. Google Pay provides faster and safer checkouts in apps and on websites, and allows users to pay for contactless transactions using their mobile phones. It is an online bank account that is part of Google Pay, offered by participating credit unions and banks. Price: Free.

4. Braintree

Braintree allows you to accept PayPal, cards or other wallets, such as Venmo (U.S.), Apple Pay, and Google Pay and also provide purchase today and pay later options. Accept payments in-person using various PayPal Here card readers by connecting with the PayPal Here SDK into your mobile point of sale app. Select from the basic or advanced fraud tools and add 3-D Secure as another layer of prevention. Securely save billing information to allow payment repeats. Cost: 2.59% + 49C for each transaction.

5. Venmo

Venmo can be described as an mobile peer-to-peer payments service that is owned by PayPal. Business profiles permit Venmo clients to receive payment for services and goods from customers who use Venmo. Customers’ accounts on Venmo are linked in applications and websites that have payment processing through Braintree. It is easy to include Venmo as an option to pay on your site. Cost: 1.9%+$0.10 per transaction.

6. Mobiyo

The Mobiyo is the European market leader in mobile payments mostly by direct carrier billing, which allows users to charge purchases through your mobile’s bill. Mobiyo also handles payments through SMS and prepaid cards, as well as electronically transferred bank funds, payments and credit card transactions, e-wallet and much other options. You can access advanced analytics to assess the performance of your account. Contact us for prices.

7. The QuickBooks GoPayment

QuickBooks GoPayment has an application and a mobile card reader that allows you to pay promptly. Accepts all major credit and debit cards. Make use of QuickBooks card reader QuickBooks Card Reader to make digital wallet transactions or manually input card information using the GoPayment application. You can access the entire range of QuickBooks tools to control your cash flow, invoices and expenditures. Price 1 cent for ACH bank transactions 2.4 percent for swiped for transactions, per transaction.

8. Zelle

Zelle can be a simple method to transfer cash directly from U.S. bank accounts, generally within minutes. Fast, securely easily transfer and receive cash using the use of an email address, or mobile number. To make use of Zelle your bank, it should offer it to your account for business. Ask your bank about pricing and availability.

9. Payanywhere

Payanywhere is a point of sale software, hardware as well as business tools that allow you to accept credit cards and manage your business. Utilize a device from Payanywhere to take payments at your physical store or via your tablet or smartphone. Convert any transaction that is in person to an invoice using the Payanywhere app, or transfer it directly from the website. With two options for funding select when your company is able to be funded by daily credit sales. Pricing: 2.69% per transaction.

10. Authorize.net

Authorize.net helps merchants accept credit card transactions in person, on the internet or by phone. Virtual point of sale is a way to connect a compatible credit card reader to your computer in order to accept payment in-store. Accept all forms of payment including major credit cards, signature debit card and electronic checks. Accept and pay monthly recurring installment payments. Pricing: 2.9% + 30C for each transaction.

11. Stripe

Stripe allows merchants to be able to accept payment and run their business online. Combine offline and online channels using flexible tools for developers including card readers, Cloud-based Hardware Management. Utilize this SDK for integration of Stripe into apps for mobile and online to design a custom checkout process. Create a marketplace, and let sellers or service providers worldwide. Cost: 2.9% + 30C for each transaction.

12. Adyen

Adyen lets merchants accept payments through one system that works for mobile, online and points of sale. Accept mobile wallets, cards and more via any device or digital channel. Design optimized checkouts for shopping with mobile and in-app payment flows. Benefit from a variety of tools that can help you assist your customers. Securely save your customers’ previous used data on payment. nd make sure they keep coming to you with one-click and regular payments. Contact us for prices.

13. Boku

Boku is created in 2009 to allow purchases of digital content from mobile phones. It was in the year 2021 that Boku announced its M1ST Payments Network that combines the mobile wallet and billing services of carriers to create a single payment scheme, with 225+ mobile payment options in more than 70 countries. Boku includes subscription bundling along with mobile identity, as well as an array of security tools. Contact us for prices.

14. WeChat Pay

The WeChat Pay is a payment function built into the China-based WeChat application that is used by more than 1 billion monthly users across the globe. WeChat offers the QuickPay featureincludes QR codes payment online, in-app payments via web and native in-app payments and mini-programs for payments. Price The merchant processing fee is 0.6 percent per transaction.

Conclusion

This is all you need to know about mobile wallets and payment using them. Now, if you are someone who wants to develop a market leading one for your own business, all you need to do is reach out to an mobile wallet app development company.